HIDDEN IN PLAIN SIGHT: CONCENTRATED STOCK RISK

From Wealth Creation to Wealth Protection

By: Stacy Hendler, Director of Portfolio & Wealth Advisory; Robert Pierce, Portfolio Strategist; Gazelle Summe, Director of Portfolio & Wealth Advisory

July 2026

__________________________________________________________________________________________

For families whose wealth derives from a single concentrated stock, the story is often a familiar one: a company they founded, equity earned over a career, shares accumulated as an early employee of a successful venture, a family business that went public, or one holding that compounded for decades. Interestingly, the very position that created the family’s wealth can also become its largest unmanaged risk. This piece lays out how we think about concentrated stock risk, what the long-term evidence shows, and the range of approaches we use to help clients understand and manage that risk.

In our experience, managing concentration risk is rarely about finding a single solution. It is about balancing risk, taxes, liquidity, and long-term objectives in a way that reflects each family’s circumstances and preferences. BBR’s role is to help families evaluate those trade-offs, understand the magnitude of their exposure, and develop a strategy aligned with their goals. Often, the objective is not to eliminate concentration risk entirely, but to build enough diversified wealth that a family’s future is no longer dependent on a single holding.

1. The Concentration Problem

A large, low-cost position in a single stock is usually the result of good decisions, hard work, and some amount of luck. The wealth is real, and the attachment to it is understandable. The mistake is assuming that the same concentration that created wealth is the right one to preserve it.

BUILDING VS. PROTECTING

A concentrated position can be a path to substantial wealth creation, but it can also become a significant source of risk once the wealth has been created. At that stage, the objective shifts from maximizing the upside to ensuring that no single event can undo it. Recognizing that the goal has changed is the most important step. For some investors, that means reducing a concentrated position substantially. For others, it means building sufficient diversified wealth around it so that future outcomes are no longer dependent on a single holding.

WHY DIVERSIFYING IS SO DIFFICULT

If diversification makes sense on paper, why is it so difficult in practice? The obstacles are rarely financial; they are almost always emotional and behavioral.

- Familiarity feels like safety: Investors may perceive a company they know well as less risky.

- The position becomes an identity: When it is linked to a career, entrepreneurial success, or family legacy, reducing it can feel like disloyalty rather than prudent planning.

- Anchoring and regret: Investors anchor to past highs, resist selling below a prior peak, and fear selling just before another run.

- Taxes loom larger than risk: The visible, certain cost of capital gains tax tends to overshadow the larger but less visible risk of staying concentrated.

These instincts are powerful and worthy of consideration. The long-term record on individual stocks is nonetheless sobering and worth confronting directly.

A common and reasonable response is to believe that the statistics apply to other stocks, not this one. The investor knows the management team, understands the competitive dynamics, and has watched the business for years. That familiarity is real, and it may even be accurate. The issue is not whether the company is good; it is whether a single company, however strong, should determine a family’s financial future. The goal of diversification is not to bet against the position. It is to help ensure that being wrong, even partially and temporarily, does not cause permanent damage.

MOST INDIVIDUAL STOCKS HAVE NOT BEATEN CASH

In one study, Professor Hendrik Bessembinder¹ examined U.S. common stocks from 1926 to 2025. Most individual stocks underperformed one-month Treasury bills over their lifetimes, with only about 43% clearing that low hurdle. Strikingly, the entire net wealth created by the U.S. stock market above Treasury bills was attributable to roughly the best-performing 4% of companies. The market rises over time, but the returns have been driven disproportionately by a small number of exceptional companies; most stocks have not matched the market’s overall performance.

MANY FACE PERMANENT IMPAIRMENT

A long-running analysis by J.P. Morgan² tells a similar story. Across thousands of stocks in the Russell 3000 between 1980 and 2020, more than 40% experienced a “catastrophic stock price loss,” defined as a decline of 70% or more from peak with no meaningful recovery, and roughly two-thirds underperformed the index itself. The danger is not merely a bad year; it is a permanent impairment that patience does not repair. No one can reliably identify in advance which stock is the rare winner and which will be the eventual casualty.

The summary we share with clients is this: the very outcome that built a concentrated position–one stock dramatically outperforming–is statistically rare and difficult to repeat. Yesterday’s winner is not guaranteed to be tomorrow’s. Reducing a portion of that exposure lessens the idiosyncratic risk associated with a single company.

2. How One Position Can Dominate a Portfolio

The case for diversification is not a matter of opinion; it follows directly from the way portfolio risk is measured. A concentrated position does not simply add risk in proportion to its size; it can dominate how the entire portfolio behaves.

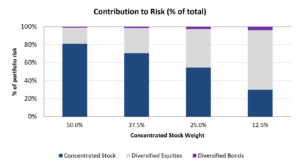

RISK SHARE, NOT CAPITAL SHARE

The natural way to size a position is by its share of portfolio value: a stock worth half the assets is “half the portfolio.” Risk, however, is distributed very differently. A volatile single stock can contribute far more to total portfolio risk than its dollar weight implies, because its swings are proportionately large and largely undiversified. In illustrative modeling we use with clients, a position representing half of assets can account for more than 80% of total portfolio risk. At that point, the portfolio’s potential outcomes are inextricably tied to a single company. Even when a stock’s position is reduced to 10% of assets, it can still constitute roughly 20% of total portfolio risk.

Source: BBR Partners

THE RANGE OF OUTCOMES WIDENS

Single stocks are more volatile than a diversified basket of companies and more exposed to company-specific risks (a product flop, an adverse regulatory ruling, employee fraud, technological disruption from a competitor). Spreading capital across many companies and sectors cushions any one setback with other holdings; a concentrated position has no such cushion and bears the full weight of one company’s fate. That exposes investors to significant downside risk, as many companies eventually face competition or disruption that permanently reduces their earnings potential.

WHAT DIVERSIFICATION DOES

One reason diversification works is that assets do not move in perfect lockstep. When holdings are less than perfectly correlated, their independent fluctuations partially offset one another, and overall portfolio risk can fall below what would be expected from a simple average of their individual risks. The practical effect is a narrower range of potential outcomes:

- The left tail shrinks: Spreading capital across many companies and asset classes makes a total, unrecoverable loss less likely. No single failure is decisive.

- Outcomes become more reliable: The path tends to smooth out. Investors are less likely to be forced to sell at the worst moment, and compounding works from a steadier base.

- Risk-adjusted return can improve: Reducing single-company risk that markets do not reward tends to raise return per unit of risk, even when expected return moderates.

We are candid with clients about the trade-off. Diversifying away from a large winner usually means giving up some potential upside and, in taxable accounts, often realizing gains. In return, it exchanges a wide, fragile range of outcomes for one that is narrower and more resilient. For wealth that already exists and is intended to last across generations, we generally view that as a worthwhile trade-off. The practical question is how to get there efficiently, which is where strategic planning and the thoughtful use of available tools matter most.

3. Approaches to Diversification

Once the decision to reduce concentration risk is made, the next question is how. Reducing a concentrated position rarely means selling everything at once and absorbing a large tax bill in a single year. A range of approaches can spread sales over time, hedge the position, or defer taxes. For some investors, particularly those who inherited a concentrated position, a stepped-up basis may reduce the tax cost of diversification and expand the range of available options. Each approach carries its own trade-offs in cost, complexity, and tax treatment, and several involve intricate rules.

There is rarely a single “best” solution. The right combination depends on the family’s tax situation, time horizon, and desire to maintain some exposure to the position. Most plans we design layer several of these approaches. The descriptions below are general.

INVESTMENT TOOLS

- Tax-loss harvesting separately managed account: A separately managed account holds a diversified basket of securities and systematically realizes losses on individual positions over time. Those losses can help offset gains realized as the concentrated position is trimmed, allowing more of it to be diversified for a given tax cost.

- Programmatic selling: Selling in scheduled increments over multiple years spreads the tax impact and removes emotion from timing. A pre-established plan, including a Rule 10b5-1 plan for corporate insiders, helps maintain discipline.

- Exchange funds: An investor contributes the concentrated stock into a pooled vehicle alongside other investors with their own concentrated holdings, receiving a diversified interest in the combined pool. This can achieve diversification on a tax-deferred basis but is typically subject to a multi-year lock-up and eligibility requirements.

PLANNING TOOLS

- Charitable gifting: Donating low-basis shares to a donor-advised fund or directly to a charitable organization can reduce a concentrated position while advancing philanthropic objectives. Because the recipient is tax-exempt, embedded capital gains may be avoided when the shares are ultimately sold.

- Charitable remainder trusts (CRTs): An investor contributes the concentrated stock to the trust, which can sell it without an immediate capital-gains tax and reinvest the full proceeds in a diversified portfolio. The trust pays the investor an income stream for a term while the remainder passes to a chosen charity. This diversifies the position and provides income, while the gain is recognized gradually over time rather than all at once.

HEDGING TOOLS

- Protective collars: Purchasing a put option establishes a floor under the stock, while selling a call option caps the upside and helps fund the put. The result is a defined range of outcomes, useful when an investor seeks protection but is not ready to sell.

- Covered calls: Selling call options against the position generates income and a modest cushion. This does not protect against a large decline, but it can help reduce a position gradually as shares are called away.

- Variable prepaid forwards: An investor receives cash today in exchange for delivering a variable number of shares later, with built-in downside protection and a capped upside. This can provide liquidity and a hedge while deferring a sale and capital gain recognition, though the tax treatment is complex and must be structured carefully.

No single approach suits everyone, and the most effective plans typically combine several, tailored to an investor’s tax situation, liquidity needs, time horizon, and willingness to part with the position. The objective throughout is consistent: to narrow the range of potential outcomes and protect hard-earned wealth in a way that aligns with the client’s goals and comfort level.

The families who navigate concentration risk most effectively are rarely those that act fastest or sell the most. They are those that are honest about what they are actually trying to accomplish, whether that is protecting a lifestyle, funding a legacy, or simply sleeping better at night. The stock that built the wealth was the right tool for one chapter; the question worth asking now is whether it is still the right tool for the next.

4. How BBR Partners Helps

Concentrated stock presents behavioral and planning complexities that are every bit as important as investment considerations. For many families, the hardest part is getting comfortable making a change they have been putting off, sometimes for years. Every family’s relationship with their position is different, and so is the right path forward. Working alongside each family and their tax and legal advisors, we bring together the full range of investment, tax, and planning tools: quantifying how much risk a concentrated position actually contributes, modeling the after-tax impact of different reduction strategies, and designing a plan that reflects the family’s goals, constraints, and comfort. The wealth created by a concentrated position deserves an equally thoughtful plan to protect it. If this is something you are navigating, we would welcome a conversation.

1One Hundred Years in the U.S. Stock Markets

____________________________________________________________________________________________

Stacy H. Hendler joined BBR Partners in 2023 and is a Director of Portfolio & Wealth Advisory. Her responsibilities include working with clients to develop their overall financial strategy, manage their investments, and integrate their investment, tax and estate planning into a cohesive wealth management plan. Stacy is also a board member of BBR’s firm-wide impact initiatives.

Robert G. Pierce joined BBR Partners in 2023 as a Director on the Investment Research Team. As a Portfolio Strategist, Rob provides the Research team with macroeconomic insights, assists with building asset allocations and capital market expectations, and serves as a liaison to the Portfolio & Wealth Advisory team on investment opportunities, client asset allocations, and portfolio level positioning. Rob is also a board member of BBR’s firm-wide impact initiatives.

Gazelle B. Summe joined BBR Partners in 2021 and is a Director of Portfolio & Wealth Advisory. Her responsibilities include working with clients to develop their overall financial strategy, manage their investments, and integrate their investment tax and estate planning into a cohesive wealth management plan.

Connect with One of Our Advisors

IMPORTANT DISCLOSURES

This presentation by BBR Partners, LLC (“BBR”) is intended for general information purposes only. No portion of the presentation serves as the receipt of, or as a substitute for, personalized investment advice from BBR or any other investment professional of your choosing. We believe the information contained in this presentation to be reliable; however, we do not warrant its accuracy or completeness. Certain estimates, investment strategies, and views expressed are based on past or current market conditions and on information provided by third parties, which has not been independently verified and is subject to change without notice. Due to various factors, including changes in market conditions or applicable laws, the information presented may no longer reflect current opinions or positions.To the extent that any portion of the content reflects assumptions and/or projections, no such content should be construed or relied upon as an absolute probability that such an assumption or projection will prove correct or projected result will occur. To the contrary, a different result (positive or negative) can, and most likely will, occur. Materially different results could occur at any specific point in time or over any specific time period. Different types of investments involve varying degrees of risk, and it should not be assumed that future performance of any specific investment or investment strategy, or any non-investment related or planning services, discussion or content, will be profitable, be suitable for your portfolio or individual situation, or prove successful.

Neither BBR’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if BBR is engaged, or continues to be engaged, to provide investment advisory services. BBR is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. No portion of the content should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if BBR is engaged, or continues to be engaged, to provide investment advisory services. A copy of BBR’s current written disclosure Brochure discussing our advisory services and fees is available upon request or at www.bbrpartners.com.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your BBR account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) comparative benchmarks/indices may be more or less volatile than your BBR accounts; and (2) a description of each comparative benchmark/index is available upon request.

SOURCES

1 Bessembinder, Hendrik. 2026. One Hundred Years in the U.S. Stock Markets. SSRN. March 18. https://doi.org/10.2139/ssrn.6438198.

2 Cembalest, Michael. 2021. The Agony & The Ecstasy: The Risks and Rewards of a Concentrated Stock Position. J.P. Morgan Private Bank. March 15. https://privatebank.jpmorgan.com/nam/en/insights/latest-and-featured/eotm/the-agony-the-ecstasy.