A REFLECTION ON 25 YEARS

by Brett Barth, Evan Roth, Stephanie Gromek, Todd Whitenack, and BBR Partners

December 2025

Reaching a quarter century is an opportune time to take stock and clearly examine the path taken, with all its twists and turns. This feels especially fitting for a firm built with a long-term time horizon. As we close out our 25th year, we are pleased to share the narrative of how our investment approach was formed, how certain tactics have evolved as we have grown, and how our core philosophies have remained unchanged.

____________________________________________________________________________________________

BBR’s beginning

“The most important rule of trading is to play great defense, not great offense.” – Paul Tudor Jones

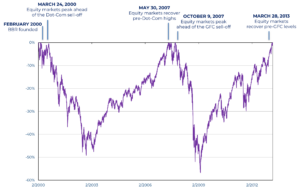

Formative experiences shape how people, businesses, and societies think about and navigate the world. Just as a child won’t understand a stove top is hot until they touch it, being warned that markets can decline is no substitute for having navigated a brutal bear market. BBR—which was founded in early 2000—was forced to touch the stove early, experiencing two of the worst equity bear markets of the past century in its first decade.

S&P 500 Drawdown; Source: Bloomberg

During the first 13 years of BBR’s history, the US equity market was in a drawdown 99.4% of the time. That impacted the firm’s formative psychology and informs how we approach managing client wealth to this day. First, do no harm; our clients have generated meaningful wealth and losing substantial capital will harm them more than making money will help them. Academic research and empirical evidence back this up; while everyone is different, on average, a loss feels twice as bad as an equivalent gain feels good. This is especially true for people with significant wealth, who have far more to lose than to gain. The key to compounding wealth over the long term is avoiding catastrophic loss, but for an agreed upon level of risk, we aim to maximize returns.

Our job is to compound capital at a reasonable rate of return, not to assume undue risk in pursuit of outsized gains. We want to avoid outsized losses, but the only way to generate attractive returns is to shoulder—and manage—risk. Fortunately, consistently generating solid returns can put investors in the upper-echelons of long-term performance. Emblematic of this dynamic is Howard Marks’ story about David VanBenschoten, the head of the General Mills Pension Fund:

“Dave told me that, in his 14 years in the job, the fund’s equity return had never ranked above the 27th percentile of the pension fund universe or below the 47th percentile. And where did those solidly second-quartile annual returns place the fund for the 14 years overall? Fourth percentile! I was wowed. It turns out that most investors aiming for top-decile performance eventually shoot themselves in the foot, but Dave never did.” – Howard Marks

Better times

“The first rule of compounding is to never interrupt it unnecessarily.” – Charlie Munger

The second half of our life as a firm has been an inversion of the first: risk assets have advanced in near uninterrupted fashion. From March 8th, 2013 through the end of October, 2025, the S&P 500 gained more than 340%; a return exceeding 12% per year that saw only two 20% drawdowns, one of which was the Covid bear market, which lasted only a few weeks.

The relatively smooth ride up and to the right has many investors, particularly new investors, discounting the risks of equity market investing. The riskiest time for investors is when risk is perceived to be absent; it is what leads to diminished diversification, performance chasing, and the use of leverage.

We believe we have done a good job participating in markets without throwing caution to the wind. Risks can’t be avoided, but they can be managed. Managing risk doesn’t mean timing the market, as a recommendation to sit in cash is counterproductive, only outperforming a diversified portfolio in the worst market selloffs. More pernicious than underperformance is the psychological whiplash that occurs from attempting to get in and out of the market, and the hesitancy to do so if you’ve missed out on market gains. As Peter Lynch observed, “far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” We have observed that the biggest risk to client objectives stems from hesitancy to be invested, not from underperforming a benchmark. A more appropriate strategy, and one we have employed, is to modulate asset class exposures based on go forward return expectations, not which assets have performed best recently. This allows portfolios to maintain market exposure without letting risk get out of hand.

BBR has navigated a quarter century of market gyrations by focusing on diversification, mean reversion, and price sensitivity.

- Diversification: the only free lunch in investing, diversification can reduce portfolio risk without sacrificing return potential. It also means always having to apologize for something, as a well-diversified portfolio, by definition, holds assets that are uncorrelated with one another.

- Mean reversion: markets tend to exhibit mean reversion over time as regimes and leadership shift and evolve. Rebalancing helps maintain the desired amount of risk and improve returns.

- Price sensitivity: the price you pay for a security informs the type of returns you can expect. Even amazing companies can be bad investments if the entry price is wrong.

Full picture

“The single greatest edge an investor can have is a long-term orientation.” – Seth Klarman

BBR has endeavored to stay levelheaded through market highs and lows. The fact that losses hurt more than gains feel good is not only a psychological problem, it’s a mathematical one. A given loss requires a greater subsequent gain to breakeven, and as the loss grows, so does the required gain. A 20% decline requires a 25% breakeven gain, but a 50% loss necessitates a 100% breakeven gain. This is why downside protection is so critical to long-term compounding.

Outperforming on the downside, even if you lag in up markets, pays off even though markets advance more often than they decline. The ability to maintain an even keel and focus on the horizon amid a cacophony of information is a superpower, particularly in a landscape that is increasingly designed to distract us from the things that matter most.

For the last 25 years (2000-2024), BBR has succeeded in doing just that—generating attractive returns relative to a 60/40 passive portfolio and global equities with less than half the volatility of the S&P 500 or MSCI ACWI. The result is strong risk-adjusted performance that makes it easier for investors to maintain the peace of mind and long-term orientation necessary to achieve their financial goals.

A learning game

“If you’re certain about anything in this business, you’re wrong.” – Cliff Asness

Because investing isn’t a single-play game, it is less about being right than it is about finding small edges. Decisions underpinned by small edges can be wrong in the short-term but pay off in the long-term, much like the tendency of a flipped coin to converge to 50/50 the more turns you take. Just as Roger Federer winning 54% of his points led to winning 84% of his matches or Renaissance Technologies getting 50.75% of its trades right built the most successful hedge fund of all time, small edges lead to big wins. Building a diversified portfolio, taking advantage of mean reversion opportunities, and focusing on the price you pay builds a repeatable, behavioral advantage into clients’ financial blueprints and increases the odds they will succeed in achieving their objectives over time. As Warren Buffett famously said, “the market is a mechanism for transferring value from the active to the patient.” Behavioral guardrails are a tool to control our worst impulses and can be a significant source of portfolio returns.

The other advantage of playing a repeat game is that we get to learn from our mistakes. Heads we win, tails we learn. While our core values have remained constant, BBR has used 25 years of managing client wealth to continually refine our approach. Among the most important lessons we’ve internalized over the past 25 years include:

- Limits to diversification: diversification is critical to resilient portfolios but being overly diversified can diminish returns and limit our ability to negotiate attractive terms for clients.

- More than one kind of risk: we want to review as many investment opportunities as possible and are more comfortable passing on a good investment (Type I error) than we are making a bad investment (Type II error). Consistently doing so helps manage different kinds of risk:

- Organizational risk – e.g. fraud. Unacceptable and we aim to avoid entirely.

- Investment risk – underperformance vs. a target. Inevitable at times, but our process minimizes these odds.

- Purchasing power risk – inflation eroding portfolio value. This can be managed through appropriate risk-taking and asset allocation.

- Complexity rarely pays: complex trades don’t pay you enough to compensate for the increased risk of something going wrong.

- It does pay to be early: fundamentals matter, but only insofar as they impact supply and demand. Investing before an asset class becomes institutionalized allows early investors to be rewarded by capital flows as demand outstrips supply, pushing prices higher.

- Pursue ideas with conviction: great ideas are uncommon; when you have one, do it. The perfect trade stems from pairing the right idea with the right manager. Part of doing this successfully is having a plan to take advantage of market dislocations when they occur.

- Tax alpha: generating tax alpha is a critical ingredient to adding value as increased competitiveness and passive flows have eroded manager alpha over time.

As BBR has evolved and grown—in mindset as well as size—we’ve been able to lean on past learnings to improve client experience and outcomes. Our scale and reputation provides us the opportunity to drive fee breaks, collaborate on thematic side pockets with managers, and attract steady deal flow; advantages that accrue to our clients. We have also evolved alongside shifting market dynamics, moving away from a low net exposure hedge fund portfolio towards a more long-biased, opportunistic stance as the lost-decade of the 2000’s gave way to an elongated bull market fueled in part by fiscal stimulus and the rise of asset-light technology businesses. We have both responded to changes in market structure and stuck to our knitting: growing client capital over time without exposing portfolios to excessive risks.

Today’s environment

“The intelligent investor is a realist who sells to optimists and buys from pessimists.” – Benjamin Graham

In some ways, the emerging mania around Artificial Intelligence feels like we are back where we started 25 years ago: a potentially transformative general-purpose technology is tempting investors with a generational investment opportunity. AI has dominated equity markets since ChatGPT was released in November 2022, with the seven stocks that have become synonymous with AI—the Magnificent 7—accounting for ~60% of S&P 500 gains.

But transformative technology doesn’t unilaterally mean a transformative investment opportunity. The internet has changed our lives more profoundly than many could have envisaged 25 years ago, but the dot-com bubble still ended in tears as valuations ran away from fundamentals, exposing the Nasdaq to an 80% decline that would take 15 years to recover. Cisco, the poster child for the dot-com era and a survivor, is only now—25 years later—approaching its 2000 highs. Our experience 25 years ago helps inform our views today: we are optimistic about the potential for AI to drive economy-wide productivity enhancements and for how it could help us run our business, but the ultimate investment beneficiaries of AI adoption remain highly uncertain. Instead, we are maintaining meaningful exposure to the AI theme without getting over our risk skis. Even the Chair of OpenAI, Bret Taylor, highlights the difference between economic impact and financial return: “It is both true that AI will transform the economy, and create huge amounts of economic value in the future. I think we’re also in a bubble, and a lot of people will lose a lot of money.” While that may not materialize, the fact that it could warrants portfolio risk discipline and maintaining an allocation that allows upside without placing all your eggs in the same basket.

Despite the risks facing investors today, we are generally optimistic about what the future holds. The development of new technologies like AI and its ability to spur innovation across many sectors such as biotech, robotics, and finance offer the potential for accelerated advancement, discovery, and profitability for businesses across sectors and industries. But we are also mindful of the seismic changes that are unfolding globally today: challenges to globalization are mounting as the inequalities that have arisen from outsourcing become more apparent, countries and regions are reshoring and pivoting from just-in-time to just-in-case inventory management after Covid supply chain shocks, and aging demographics will stress government finances globally. While the net outcome is highly uncertain, change often presents attractive investment opportunities and secular themes that can benefit investors. We continue to monitor and evaluate rapidly shifting market dynamics with a focus on delivering for clients. As always, long market advances will be punctuated by dramatic drops. Investors who stay the course, lean on global diversification, and respond opportunistically without risking catastrophic loss should be rewarded. Through it all, we will maintain our hard-earned discipline in pursuit of compounding client wealth.

As we reflect on 25 years as a firm, we want to express heartfelt gratitude for the trust you have placed in us and the relationships that we have built with each of you. We could not have succeeded to the degree we have without you; our hope—and the aspiration that drives us—is that we have played a small role in your success, too.

Connect with One of Our Advisors

Important Disclosure Information: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by BBR Partners, LLC (“BBR”)), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from BBR. Neither BBR’s investment adviser registration status, nor any amount of prior experience or success, should be construed that a certain level of results or satisfaction will be achieved if BBR is engaged, or continues to be engaged, to provide investment advisory services. BBR is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of BBR’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.bbrpartners.com. Please Remember: If you are a BBR client, please contact BBR, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your BBR account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) comparative benchmarks/indices may be more or less volatile than your BBR accounts; and (2) a description of each comparative benchmark/index is available upon request.